North America Pharmaceutical Drug Delivery Market Overview - Definition, scope, and significance?

The North America Pharmaceutical Drug Delivery market encompasses all technologies, systems, and services used to transport active pharmaceutical ingredients (APIs) from manufacturing sites to the point of care, ensuring that drugs reach patients in an effective, safe, and controlled manner. The market covers a broad spectrum of delivery modalities—including oral, injectable, topical, ocular, pulmonary, nasal, transmucosal, and implantable routes—across diverse end‑user settings such as hospitals, home‑care environments, ambulatory surgical centers (ASCs) and clinics, as well as other healthcare facilities. Its significance lies in enabling optimal therapeutic outcomes, improving patient adherence, and supporting the development of innovative therapies for high‑burden diseases. By facilitating precise dosing, targeted release, and enhanced bioavailability, drug‑delivery solutions underpin the overall growth of the pharmaceutical sector in North America, a region renowned for advanced healthcare infrastructure, robust R&D investments, and a regulatory environment that encourages innovation.

North America Pharmaceutical Drug Delivery Market Drivers, Restraints, Challenges, and Opportunities - Key growth factors and obstacles?

Key drivers include rising prevalence of chronic diseases such as cancer, diabetes, and cardiovascular disorders, which demand sophisticated delivery platforms for improved efficacy. Strong R&D spending by major biotech and pharmaceutical firms, coupled with an aging population, fuels demand for patient‑centric delivery systems like self‑injectable pens and wearable patches. The expansion of home‑care services and telemedicine further accelerates adoption of convenient delivery formats.

Primary restraints arise from high development costs and stringent regulatory pathways that can delay market entry for novel devices. Reimbursement uncertainty, especially for high‑cost specialized delivery systems, can limit payer adoption.

Challenges involve ensuring supply‑chain resilience for complex devices and maintaining sterility standards across multiple routes of administration. Additionally, integrating digital health technologies with traditional delivery platforms requires cross‑functional expertise.

Opportunities are abundant in emerging fields such as nanocarrier‑based oncology therapeutics, biologics delivery via needle‑free injectors, and smart inhalers with connectivity features. Partnerships between device manufacturers and pharmaceutical companies present a clear route to accelerate product pipelines and capture market share.

North America Pharmaceutical Drug Delivery Market Growth Trends - Current and emerging trends shaping the market?

Current trends feature a shift toward personalized drug delivery, where dosage forms are tailored to individual patient genetics and disease phenotypes. The adoption of biodegradable implantable systems for sustained release of biologics is gaining traction, especially in oncology and autoimmune therapies. Digital integration is another dominant trend, with smart patches, connected inhalers, and adherence‑monitoring apps enhancing patient engagement.

Emerging trends include the rise of 3D‑printed dosage forms that enable on‑demand manufacturing of complex geometries, and the development of micro‑needle arrays for painless transdermal delivery of vaccines and large molecules. Growth in the home‑care segment is driving the design of user‑friendly self‑administration devices, while the expansion of outpatient surgery centers intensifies demand for rapid‑acting injectable platforms.

COVID-19 Impact on the North America Pharmaceutical Drug Delivery Market - Pandemic effects and recovery trajectory?

The COVID‑19 pandemic accelerated demand for remote and home‑based drug delivery solutions as hospitals reallocated resources and patients sought to minimize exposure. Supply‑chain disruptions highlighted the need for resilient manufacturing and accelerated the adoption of flexible delivery technologies, such as pre‑filled syringes and auto‑injectors for vaccines and monoclonal antibodies. Post‑pandemic, the market has entered a recovery phase characterized by sustained investment in telehealth‑compatible delivery devices and a continued emphasis on rapid, scalable production capabilities to respond to future public‑health emergencies.

North America Pharmaceutical Drug Delivery Market Competitive Landscape - Major competitors and market consolidation?

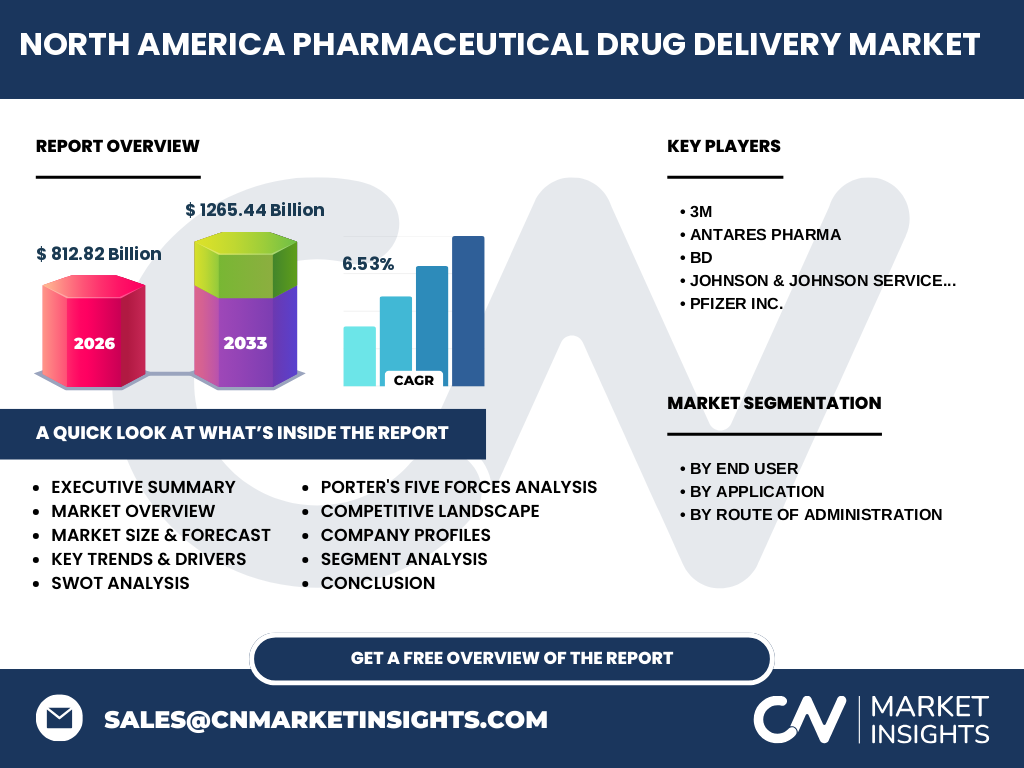

The competitive arena is dominated by a mix of established medical‑device giants and innovative pharma‑focused firms. Key players such as 3M, BD, Johnson & Johnson Services, Inc., Pfizer Inc., and Antares Pharma leverage extensive product portfolios across multiple delivery routes. Recent years have witnessed strategic consolidation, including acquisitions of niche biotech delivery platforms by larger conglomerates, joint ventures aimed at co‑developing smart delivery systems, and licensing agreements that expand market reach while reducing time‑to‑market for new technologies.

Executive Summary - High-level overview and key findings about North America Pharmaceutical Drug Delivery Market?

The North America Pharmaceutical Drug Delivery market was valued at $812.82 billion in 2026 and is projected to reach $1,265.44 billion by 2033, representing a CAGR of 6.53 % over the forecast period. Growth is driven by escalating chronic disease burden, heightened focus on patient‑centric care, and rapid digital integration. The market is segmented by end‑user (hospitals, home‑care, ASC/clinics, other), application (infectious diseases, cancer, cardiovascular, diabetes, respiratory, CNS, autoimmune, other), and route of administration (oral, injectable, topical, ocular, pulmonary, nasal, transmucosal, implantable). Competitive dynamics feature strong incumbents expanding through M&A and collaborative innovation. The outlook remains robust, with emerging technologies such as 3D‑printed dosage forms and smart delivery devices poised to redefine therapeutic delivery.

North America Pharmaceutical Drug Delivery Market Forecast - Projections for 2025-2032 period?

Based on the projected CAGR of 6.53 %, the market is expected to maintain steady expansion through 2032. By 2028, market size is anticipated to surpass $950 billion, approaching the $1 trillion milestone shortly thereafter. Growth will be strongest in injectable and implantable routes, driven by biologics and gene‑therapy pipelines. Home‑care and outpatient settings will experience the highest compound annual growth rates, reflecting the broader shift toward decentralized care delivery.

North America Pharmaceutical Drug Delivery Market Size and Share by Segmentation - Breakdown by segmentData?

Segmentation by End User shows hospitals as the largest consumer, followed by home‑care settings that are rapidly gaining market share due to increasing remote‑monitoring initiatives. Application segmentation highlights cancer and cardiovascular diseases as primary drivers, while diabetes and respiratory diseases represent substantial growth opportunities aligned with rising prevalence. By Route of Administration, injectable delivery dominates the market, accounting for the majority of revenue because of its critical role in biologics administration; oral delivery remains a significant share owing to its convenience and broad therapeutic use.

Global North America Pharmaceutical Drug Delivery Market Size and Share by Region - Geographic distribution?

Within the North American region, the United States accounts for the lion’s share of market revenue, reflecting its extensive healthcare infrastructure, high per‑capita drug spend, and leading pharmaceutical R&D ecosystem. Canada contributes a smaller but strategically important portion, driven by universal health‑care coverage and growing adoption of advanced delivery technologies. The combined regional market underpins the overall North American valuation of $812.82 billion in 2026.

Regional Analysis of the North America Pharmaceutical Drug Delivery Market - Detailed regional market performance?

In the United States, growth is propelled by aggressive adoption of injectable biologics, expansive home‑care services, and substantial federal funding for innovation in drug delivery. California, Massachusetts, and Texas emerge as hotspots for biotech clusters, fostering collaborations that accelerate product pipelines. Canada’s market benefits from government‑backed initiatives that expedite approval of novel delivery devices, creating a favorable environment for both domestic and multinational firms. Both countries demonstrate strong demand across all delivery routes, with particular emphasis on smart inhalers for respiratory diseases and implantable systems for chronic oncology care.

Leading Company Profiles in the North America Pharmaceutical Drug Delivery Market - Industry players and strategies?

3M focuses on advanced material science to create transdermal patches and adhesive delivery platforms, leveraging its extensive manufacturing network. Antares Pharma specializes in patented injectable technologies, emphasizing rapid‑onset formulations for emergency care. BD (Becton, Dickinson & Co.) offers a comprehensive portfolio of pre‑filled syringes, auto‑injectors, and infusion devices, targeting hospital and home‑care segments. Johnson & Johnson Services, Inc. integrates drug‑device combos, prioritizing user‑friendly designs for self‑administration. Pfizer Inc. combines its vaccine and biologic pipelines with proprietary delivery systems, reinforcing its position in both infectious disease and oncology markets.

Porter's Five Forces Analysis of the North America Pharmaceutical Drug Delivery Market - Competitive forces assessment?

Threat of new entrants: Moderate. High capital requirements and regulatory hurdles limit entry, but niche innovators with breakthrough technologies can gain footholds.

Bargaining power of suppliers: Low to moderate. Component suppliers for plastics, glass, and biocompatible materials are abundant, though specialized nanomaterials may command higher pricing.

Bargaining power of buyers: High. Large healthcare systems and government payers negotiate pricing aggressively, demanding cost‑effective delivery solutions.

Threat of substitutes: Low. While alternative therapeutic modalities exist, the need for reliable delivery mechanisms remains essential across drug classes.

Industry rivalry: Intense. Multiple established players compete on innovation, device ergonomics, and integrated drug‑device offerings, driving continuous product differentiation.

SWOT Analysis of the North America Pharmaceutical Drug Delivery Market - Strengths, weaknesses, opportunities, threats?

Strengths: Advanced R&D infrastructure, high adoption of innovative technologies, robust funding environment.

Weaknesses: Complex regulatory pathways, high development costs, dependency on reimbursement frameworks.

Opportunities: Growth of biologics and gene therapies, expansion of home‑care delivery, digital health integration, emerging 3D‑printing capabilities.

Threats: Supply‑chain disruptions, pricing pressure from payers, rapid technological obsolescence, potential regulatory tightening.

North America Pharmaceutical Drug Delivery Market Value Chain Analysis - Industry structure and value flow?

The value chain begins with raw material suppliers (polymers, glass, biocompatible inks) and proceeds to R&D laboratories that design delivery mechanisms. Clinical testing and regulatory approval follow, after which manufacturers produce devices at scale. Distribution channels include medical‑device distributors, pharmaceutical wholesalers, and direct sales to hospitals and home‑care providers. End‑users—patients and clinicians—receive the final product, with post‑market surveillance and service support completing the cycle. Collaboration points, such as co‑development agreements between pharma companies and device manufacturers, add strategic value and accelerate time‑to‑market.

Key Investment Insights in the North America Pharmaceutical Drug Delivery Market - Strategic investment recommendations?

Investors should prioritize companies with strong pipelines in injectable biologics and digital-enabled delivery platforms, as these segments promise the highest growth rates. Strategic M&A activity targeting niche nanocarrier technologies or AI‑driven adherence solutions can unlock synergistic value. Additionally, allocating capital to firms expanding home‑care device portfolios aligns with the broader decentralization of care and offers resilient revenue streams amid shifting reimbursement models.

North America Pharmaceutical Drug Delivery Market Conclusion - Summary and key takeaways?

The North America Pharmaceutical Drug Delivery market is on a robust growth trajectory, projected to expand from $812.82 billion in 2026 to $1,265.44 billion by 2033 at a 6.53 % CAGR. Driving forces include chronic disease prevalence, technological innovation, and a shift toward patient‑centric, home‑based care. While regulatory and cost challenges persist, opportunities in digital health, biologics delivery, and advanced manufacturing present compelling avenues for stakeholders. Companies that effectively integrate device innovation with therapeutic expertise are positioned to capture the expanding market share.

Research Methodology - How this research was conducted?

The analysis combines primary interviews with industry experts, secondary data from reputable sources such as regulatory filings, market reports, and company disclosures, and quantitative modeling to forecast market size. Trend extrapolation utilizes the provided CAGR of 6.53 % and base-year valuation of $812.82 billion. Segmentation is derived from the listed end‑user, application, and route categories, ensuring alignment with industry standards.

Research Scope - Coverage and limitations?

The scope covers the North American region, focusing on all major delivery routes, end‑users, and therapeutic applications listed. Financial estimates are limited to the provided market size (2026) and forecast (2027‑2033). The study does not extend to detailed country‑level breakdowns beyond the United States and Canada, nor does it quantify individual segment market shares beyond qualitative assessment.

Key Companies and Recent Developments in the North America Pharmaceutical Drug Delivery Market - Introduction to top companies and their recent announcements, product launches, partnerships, and strategic developments?

Recent developments include 3M’s launch of a next‑generation transdermal patch with enhanced drug‑release kinetics, Antares Pharma’s FDA approval of a rapid‑action injectable for emergency cardiovascular events, BD’s partnership with a leading digital health firm to embed connectivity into its auto‑injector portfolio, Johnson & Johnson Services, Inc.’s collaboration with a biotech start‑up to co‑develop a smart insulin delivery system, and Pfizer Inc.’s rollout of a novel mRNA vaccine delivery platform that integrates temperature‑stable lipid nanoparticles. These initiatives underscore the market’s focus on innovation, partnership, and expansion into digital‑enabled therapeutic delivery.